UK inflation has fallen unexpectedly to 1.7% in the year to September, acting as the lowest rate seen in three and a half years.

Decrease in Inflation Rate

September’s Consumer Prices Index (CPI) measure of inflation was recently released, with a figure of 1.7%, meaning that inflation is currently below the Bank of England’s 2% target rate.

What could this lower inflation rate mean for you?

More Bang for Your Buck

A fall in inflation means that prices are still increasing, but they are doing so at a slower rate than they were previously.

A lower inflation rate means we have more purchasing power than we would with a higher rate because when prices are higher, our money doesn’t stretch as far.

Lower Mortgage Rates

This lower inflation rate may pave the way for future interest rate cuts, meaning we could see lower mortgage rates in the future.

A lower inflation rate can produce knock-on effect with lower mortgage rates because inflation indirectly influences mortgage rates.

The base rate is used by the Bank of England to reduce inflation, and when inflation is higher, the base rate tends to be higher, and when inflation is lower, the base rate is often cut.

Mortgages tend to be priced to reflect what experts expect future interest rates to be. So, if inflation falls quicker than expected, it can lead to reductions in market expectations for the base interest rate, leading to lower mortgage rates being offered.

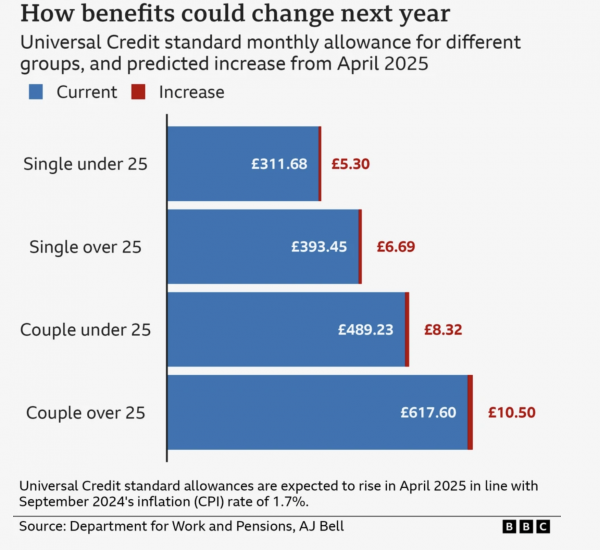

A Smaller Increase in Benefit Payments

Most benefits in the UK are inflation-linked, being increased each April based on the inflation rate from the previous September. This is to ensure that benefits are broadly kept in line with the cost of living.

Given that September’s CPI figure was lower than expected, the increase in benefits will be relatively small, rising less than some would hope. Because benefits are uprated by using a past measure of inflation, the rate of inflation could have risen above the Bank of England’s target again by the time the new tax year rolls around. So, if this low inflation rate is temporary rather than sustained, many claiming benefits will be worse off.

Universal credit is among other benefits expected to rise with inflation. According to AJ Bell, the standard allowance of universal credit for a single person under 25 is expected to rise by £5.30 a month to around £317.

However, the State Pension will not be affected by a lower inflation rate because it is guaranteed by the triple lock, increasing each April in line with whichever of the following rates is the highest:

- Earnings growth

- Inflation (measured by CPI)

- 2.5%

This time around, the highest of these figures is earnings growth, coming in at 4.1%, meaning that is the rise that State Pensions will see in the new tax year.