The Bank of England (BoE) is looking into the creation of a digital pound that could be used for in-person or online purchases, acting as an alternative for (but not a replacement of) cash.

The Digital Pound

The central bank digital currency (CBDC) or ‘digital pound’, would use some of the same technologies as cryptocurrency. However, it would be different in nature as it would have a central regulator (BoE) and its value would be denominated in pound sterling, rather than being entirely demand and supply driven.

Why is it being Considered?

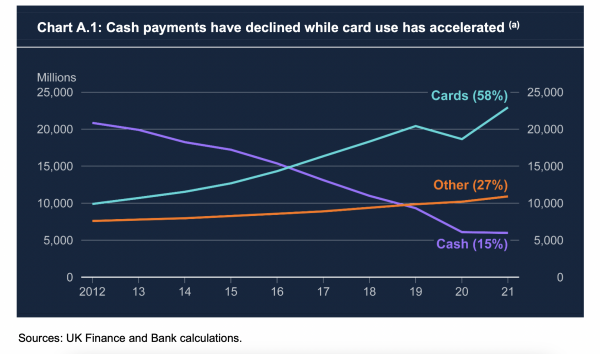

According to BoE’s February 2023 Consultation Paper, banknotes are not being used as much by households and businesses.

From the above graph, taken from page 9 of said paper, we can see the decline of cash use in recent years, combined with an increase in card purchases.

Therefore, introducing digital money could be a way to take into account these consumer trends.

Perhaps here we can link the impact of Covid-19. During the height of the pandemic, we saw many businesses unwilling to accept cash payments due to it being less sanitary. Perhaps this has now stimulated a change in consumer purchasing wherein we are now less likely to resort to cash because we saw the ease of which we could live without it.

BoE has stated, “while we ensure continued access to cash, we also have to recognise that it cannot be used in digital transactions.” The proposed digital pound is not intended to replace cash, but rather to act as an alternative when cash cannot be used, or when consumers do not wish to use it.

Critcism

Moody’s Investors Service have argued that CBDCs would disrupt traditional banks. This in turn could lead to closure of branches and job losses as a result, due to the shift in the power structure of financial institutions.

The House of Lords Economic Affairs Committee produced a report called ‘Central bank digital currencies: a solution in search of a problem,’ by which their title sums up their findings: that the digital pound is unnecessary.

Lord Forsyth of Drumlean, Chair of this Committee, stated, “We took evidence from a variety of witnesses and none of them were able to give us a compelling reason for why the UK needed a central bank digital currency. The concept seems to present a lot of risk for very little reward. We concluded that the idea was a solution in search of a problem.”

The ICAEW also stated that, “the shift in banking practices away from consumers holding money in cash form or as commercial bank deposits carries potentially seismic risks from a financial stability and monetary policy perspective.” However, BoE aims to address the risk to financial stability by setting deposit limits of £10-£20k in order to reduce money flows from commercial banks.

As you can see, the digital pound is certainly not an uncontested idea, as many have concerns about its potential repercussions. Perhaps one of the largest concerns from the public is about potential breaches of privacy…

Privacy

In response to these privacy concerns, BoE states that the digital pound would be “subject to rigorous standards of privacy and data protection.” They have proposed a platform model wherein Payment Interface Providers would identify and verify users but then anonymise this personal data before sharing information with the Bank. Therefore, neither BoE nor the Government would have access to users’ personal data, except for in exceptional circumstances whereby law enforcement agencies would be legally entitled to. This proposed system would therefore work similarly to current digital payments and bank accounts.