The Government has recently launched an 8 week public consultation regarding the regulation of the Buy Now Pay Later (BNPL) credit industry.

An Overview of BNPL

BNPL firms tend to offer short term interest free loans to enable customers to spread out payments for their purchases.

Because repayment instalments are free, BNPL financing can reduce consumers’ perceived risk of debt, encouraging them to spend money they don’t actually have.

BNPL financing is largely unregulated, with many consumers unaware of the potential consequences of missed payments.

The Stats…

According to Equifax, at least 15 million people in the UK currently use BNPL purchasing, with 1/3 of those spenders falling in the 20-30 age category.

Adobe Analytics found that purchases made using BNPL services made up 12% of online orders this January, compared to 10.7% in January 2022. We can clearly see that more and more consumers are turning to BNPL, seeking to spread the costs of their purchases due to being unable to afford them at the moment of buying.

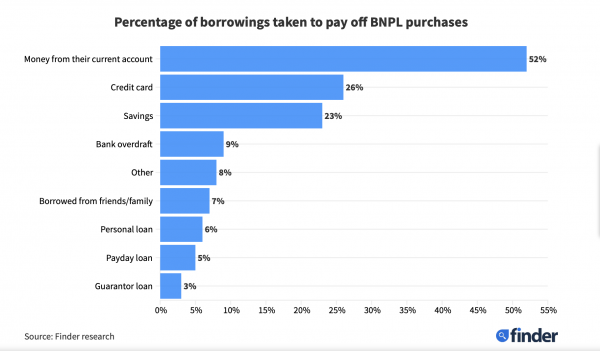

The above graph, courtesy of Finder, illustrates the problems that arise with BNPL, with many turning to further borrowing to pay what they owe to these firms. This can be seen with 26% using their credit card to pay off BNPL purchases, 9% accessing their bank overdraft and 14% taking out other forms of loans (personal, payday and guarantor).

The Promise of Protection

Regulation of the BNPL sector has been discussed since 2021, so it is long overdue. As stated by Claer Barrett, author of What They Don’t Teach You About Money, “compared to the booming nature of Buy Now Pay Later, the pace of regulation has been glacially slow.”

As it currently stands, BNPL agreements involve minimal credit checks with a lack of requirement for lenders to supply important information about their loan agreements to borrowers. This enables consumers to get into a situation where they are borrowing more money than they can actually afford to repay.

This Tuesday, on 14th February 2023, ministers launched an 8 week consultation into the regulation of the BNPL credit industry. New proposals would mean BNPL products would be regulated by the Financial Conduct Authority, with consumers able to report complaints to the financial ombudsman.

Once given new powers to regulate the BNPL industry, the FCA will consult on rules for the sector to follow, such as mandatory affordability checks, licensing of operators, and fair marketing.

The Government has estimated that 10 million consumers could be protected from “unconstrained borrowing” as a result of these measures.

To access the consultation on this draft legislation of BNPL regulation, click here.